Costco Wholesale (NASDAQ: COST) and Amazon (NASDAQ: AMZN) are both categorized as retail stocks, but their varied business models make for some challenging comparisons when trying to determine which is the better investment.

One commonality is that both companies are leaders in their respective areas of retail (Costco leads the wholesale brick-and-mortar sector and Amazon is the king of e-commerce). Costco has vastly expanded its online presence in recent years so some comparisons are getting easier. Likewise, Amazon is building a position in grocery stores with its subsidiary Whole Foods.

One significant commonality is that they both use a subscription-based model to increase sales and encourage brand loyalty. Costco has found considerable success in offering an annual membership for access to its super competitive product pricing. Amazon’s Prime membership gives members access to cheaper and more efficient shipping (as well as other perks). Both companies boast an impressive renewal rate on these memberships. These subscription models pave the way for reliable growth over the long term, helping both companies worry less about product sales and more about membership growth.

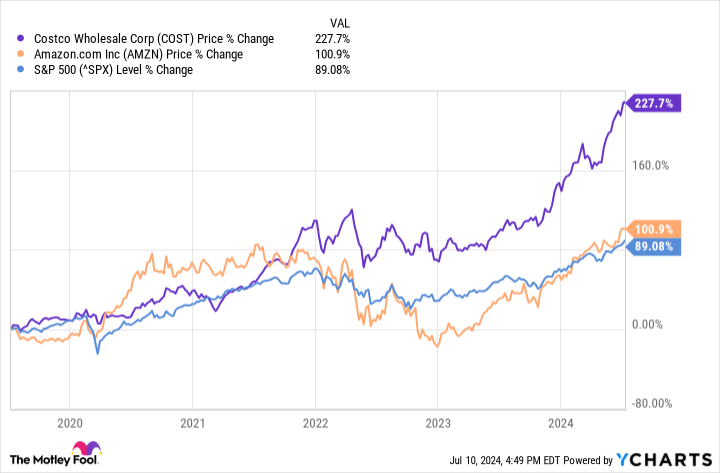

On the investor side, that steady income is attractive and it has helped both Costco and Amazon stocks deliver market-beating gains over the past several years (see chart above). Even better, both stocks are expected to continue this above-average performance, offering new investors a chance to get in on the continued growth.

But if you only had room to add one of these retail stocks to your portfolio, which should you choose? Which one has a better chance to profit from the retail sector’s continued growth over the next decade?

The case for Costco

As measured by market cap, Costco (at $390 billion) is the world’s third-largest retailer (trailing only Amazon and Walmart). The company has come a long way during the nearly 50 years it’s existed. Costco now operates 879 warehouses across 14 countries. Yet it has barely scratched the surface of its expansion potential.

Costco’s relatively unique business model offers paying club members access to wholesale prices on thousands of products across multiple categories. The company’s priorities emphasize quality products and low-margin prices catered to the varied cultures of the countries it operates in. Its earnings continue to rise despite its low margins and investments in international expansion thanks to efficient operations, loyal customers, and steady membership fees.

Over the past five years, Costco’s annual revenue and operating income have jumped 59% and 71%, while free cash flow has soared by 121%. For reference, Walmart’s free cash flow fell 14% during the same period.

And despite its steady growth (including achieving 714 locations in North America), the retail giant still has plenty of room to add more stores and grow its footprint. Costco has seven or fewer stores in six of the 14 nations it operates in, suggesting it’s only just getting started in those markets. Its expansion will only be helped by the 91% membership renewal rate the company has worldwide, which saw it hit 128 million members in 2023.

Moreover, e-commerce has become a major growth catalyst for Costco in recent years. In the third quarter of 2024, e-commerce sales rose 21% year over year, more than double the growth from any other segment and even outperforming Amazon’s retail growth in the same quarter.

As already noted, investors are attracted to Costco’s business model. As a result, shares in Costco have delivered triple-digit growth over the last five years. That elevated share price performance has also elevated the stock’s valuation well above its 10-year average. That elevated valuation is reasonable, though, given its growth potential.

The case for Amazon

Like Costco, Amazon has amassed a considerable user base. Its subscription-based model has seen Amazon Prime gain over 200 million subscribers worldwide, boasting a 99% 2-year renewal rate in the U.S. Prime has become so ubiquitous that roughly 71% of all U.S. Amazon shoppers are members.

Amazon’s annual revenue and operating income have risen by 105% and 153%, respectively, over the last five years, and its free cash flow is up 111%. That growth has come despite the economic turbulence of 2021 and 2022, proving the resiliency of Amazon’s business.

However, Amazon’s overwhelming presence in online retail has caused e-commerce growth to slow, with sales in Q1 2024 up 5% compared to total revenue growth of 13% year over year. As a result, the company has steadily reinvested its gains into diversifying its revenue streams, becoming one of the most prominent names in tech. The company is home to the world’s biggest cloud platform, Amazon Web Services (AWS), and is responsible for a leading 22% market share in video steaming thanks to the success of Prime Video.

While retail continues to deliver sales growth, the company’s positions in cloud computing and streaming are boosting earnings even more. In the first quarter, AWS revenue spiked by 17% year over year, while operating income nearly doubled. Meanwhile, advertising services sales jumped 24% year over year after Amazon introduced ads on Prime Video.

Amazon has built itself into a behemoth in retail and tech. The growth catalysts across both industries make its stock worth considering. Its valuation is elevated compared to an average stock, but low compared to other tech stocks and not bad compared to its 10-year average. Given its growth potential going forward, its valuation is reasonable.

Is Costco or Amazon the best stock to buy right now?

As was noted at the top, comparing these two stocks isn’t easy. They really are different companies with different factors influencing the investment thesis for each. Finding financial metrics that allow for fair comparisons isn’t easy either. How do you fairly compare what is best described as a tech growth stock to what is best described as a retail sector dividend stock?

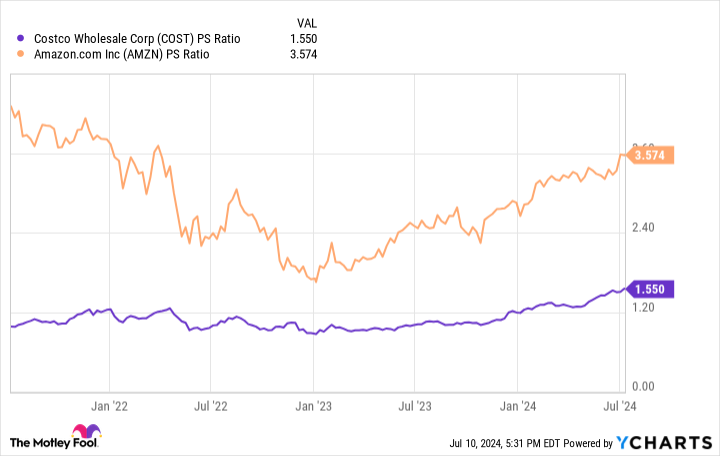

Even a basic metric like the price-to-sales ratio (P/S) isn’t perfect. The chart below would seem to indicate Amazon is the more expensive stock to buy right now.

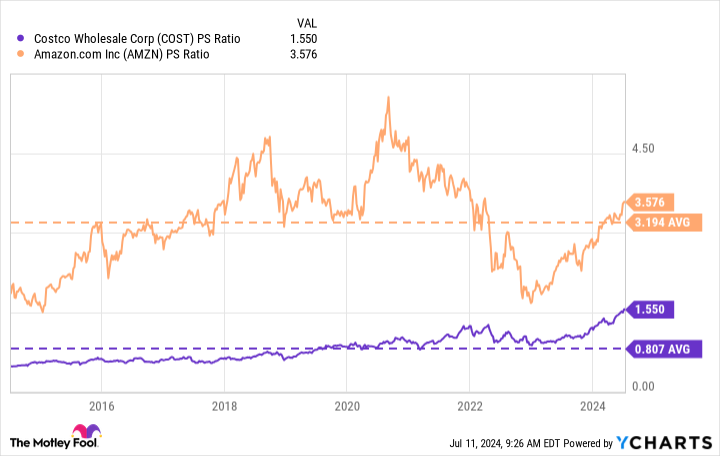

But expand that chart out over a decade and include 10-year averages, and you see that the answer is more complicated. Amazon stock is actually trading around its average P/S while Costco is trading roughly twice its average P/S over the past decade. That suggests Costco is the more expensive stock.

It’s fair to say that both Costco and Amazon are killing it in their respective industries, and both companies’ stocks are likely to lift any portfolio over the long term. So the choice between these companies really comes down to your investment style.

Another look at the chart above shows that Amazon’s P/S has been erratic over the past decade, while Costco’s has remained more stable. Amazon’s focus and earnings are gradually moving away from retail and more into tech, an industry that generally offers significant gains over the long term but can also suffer short-term steep declines from time to time. Costco has offered more reliable growth.

So, if you’re willing to hold during potential market downturns in order to gain exposure to high-growth markets like cloud computing, artificial intelligence, and digital advertising, Amazon stock is an excellent option. If you prefer a steady growth stock (also offering a dividend) that you can just buy and forget about over the next decade, you might be better suited to Costco’s stock.

Given my investing goals and interests, Amazon is the better buy than Costco at the moment.

Should you invest $1,000 in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $791,929!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 8, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Dani Cook has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Costco Wholesale, and Walmart. The Motley Fool has a disclosure policy.

Best Stock to Buy Right Now: Costco vs. Amazon was originally published by The Motley Fool