(Bloomberg) — The bond trade that some of Wall Street’s biggest banks say will dominate the rest of 2024 is gaining steam before a crucial inflation reading that will help seal the wager’s fate.

Most Read from Bloomberg

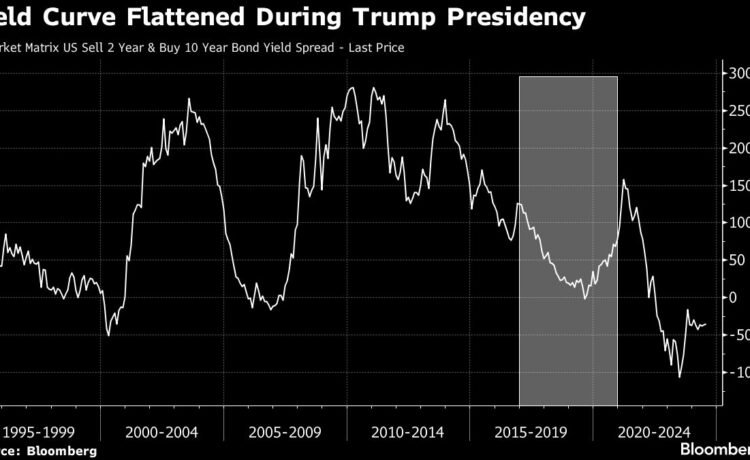

The bet — that the US yield curve will normalize toward a steeper slope — is suddenly looking as good as it has in months.

It got an initial boost after President Joe Biden’s June 27 debate performance appeared to ease Donald Trump’s path to retake the White House. In its aftermath, strategists at banks including Citigroup Inc., JPMorgan Chase & Co. and Morgan Stanley have touted the so-called Trump trade. The idea is that the Republican’s policies on tariffs, immigration and deficits will lead investors to demand higher yields on longer-maturity Treasuries.

The next leg up in the trade came Friday, when fresh signs of a softening job market bolstered expectations that the Federal Reserve will cut interest rates this year, spurring a sharp drop in short-dated yields. One closely watched measure of the yield curve — the gap between 5- and 30-year yields — reached the widest since February after the data.

Easing by the central bank is seen as the steepener bet’s principal driver, which heightens the focus on inflation readings ahead this week. Consumer prices likely rose at the slowest annual pace since January, a Bloomberg survey shows. Evidence of further disinflation may remove a major obstacle to the steepener’s success: Fed officials have been signaling that they’re not ready to lower rates.

“The steepening because of inflation, because of fiscal policy, can continue,” said Cindy Beaulieu, chief investment officer for North America at Conning.

The trade was a market favorite around the turn of the year as well, as investors entered 2024 betting on a series of Fed rate cuts. Instead, a resilient economy and sticky inflation derailed wagers on easing. When the US bond market closed on June 27 hours before the debate, the difference between 5- and 30-year yields was about 5 basis points narrower relative to the end of the year. The trade, in other words, was a loser.

While political developments initiated its revival, a more sustainable move requires the Fed to cut aggressively. That would push short-term yields down more than those on longer tenors, producing what traders call a bull-steepening move.

What Strategists Say…

Though steepening of the Treasury yield curve may continue in the short term, we think recent bear steepening may soon conclude in favor of bull steepening once the Fed begins its rate-cut cycle… Though there are periods when the yield curve bull or bear flattens, the large moves in the curve are related to how the front end moves, suggesting Federal Reserve policy is key to the direction of the yield curve.

—Ira Jersey and Christopher Cain. Read more here.

But there are few signs that the economy is fading to a degree that would trigger an imminent rescue from the Fed. Nor do policymakers seem to be confident enough that inflation is cooling sufficiently.

“When we look at recent jobs and inflation data, we do not see the case for a lot of cuts this cycle,” said Baylor Lancaster-Samuel, chief investment officer at Amerant Investments Inc. “There’s certainly a risk that this Fed will continue to hold rates at a restrictive level well into 2025. So the risk is that we don’t get that aggressive bull steepening anytime soon.”

Goldman Sachs Group Inc. strategists are also skeptical toward the steepener. They expect the 5- to 30-year gap to be basically unchanged in the fourth quarter from current levels.

Strategist Bill Zu points out that when Trump initiated the trade war with China during his presidency, yields declined and the curve flattened as tariffs weighed on productivity and growth. In addition, the relatively small difference in the outlook for US deficits under the two candidates’ policies suggests that any supply-driven yield repricing based on the election should be “modest at best,” he said.

On the other end of the spectrum, strategists at TD Securities anticipate that the spread between 5- and 30-year yields will eventually quadruple from now, to 100 basis points. Fed cuts are integral to that call, which the bank has held since last year. But so is the threat of high deficits no matter which party prevails in November, TD’s Gennadiy Goldberg and his team wrote late last month.

Greg Wilensky, head of US fixed income at Janus Henderson Investors, said he’s “moderately” positioned for a steeper curve by being overweight the five-year part of the curve and underweight longer maturities. The state of the economy will be the main trigger for the strategy, rather than politics, he said.

“The data that we’re going to see is going to, hopefully, increase the probability that a soft landing can be achieved, and the Fed can start cutting rates,” he said. “That’ll be good for steepeners.”

What to Watch

-

Economic data:

-

July 8: New York Fed 1-year inflation expectations; consumer credit

-

July 9: NFIB small business optimism

-

July 10: MBA mortgage applications; wholesale inventories

-

July 11: Consumer price index; real average earnings; weekly jobless claims; monthly budget statement

-

July 12: Producer price index; University of Michigan sentiment

-

-

Fed calendar:

-

July 9: Vice Chair for Supervision Michael Barr; Chair Jerome Powell testifies to Senate Banking and Housing Committee; Governor Michelle Bowman

-

July 10: Powell testifies to House Financial Services Committee; Chicago Fed’s Austan Goolsbee and Bowman; Governor Lisa Cook

-

July 11: Atlanta Fed’s Raphael Bostic; St. Louis Fed’s Alberto Musalem

-

-

Auction calendar:

-

July 8: 13- and 26-week bills

-

July 9: 42—day CMB; 52-week bills; 3-year notes

-

July 10: 17-week bills; 10-year notes reopening

-

July 11: 4- and 8-week bills; 30-year bonds reopening

-

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.