It’s hard to deny that Nvidia and artificial intelligence (AI) have been the story of Wall Street through the first six months of 2024. Nvidia’s meteoric rise from soaring demand for its AI chips has turned the stock into a multitrillion-dollar beast that has made shareholders very wealthy in a short amount of time.

But even the best things don’t last forever. I’m not predicting Nvidia’s downfall, but it makes sense to start looking for the next winner at a certain point. Snowflake (NYSE: SNOW) doesn’t jump out as an obvious choice — shares have fallen over 35% since January. However, the market might have gotten this all wrong.

I’ll detail below why Snowflake’s future is bright and why the stock could outperform Nvidia over the remainder of 2024.

From hype to the trash heap

Snowflake went public in late 2020, near the peak of a euphoric stock market that snatched up growth stocks due to zero-percent interest rates. Investors saw Snowflake as a cutting-edge technology company; its cloud-based platform enables customers to securely store, search, and integrate their data with various third-party apps. Even Warren Buffett got involved, whose company, Berkshire Hathaway, participated in the IPO.

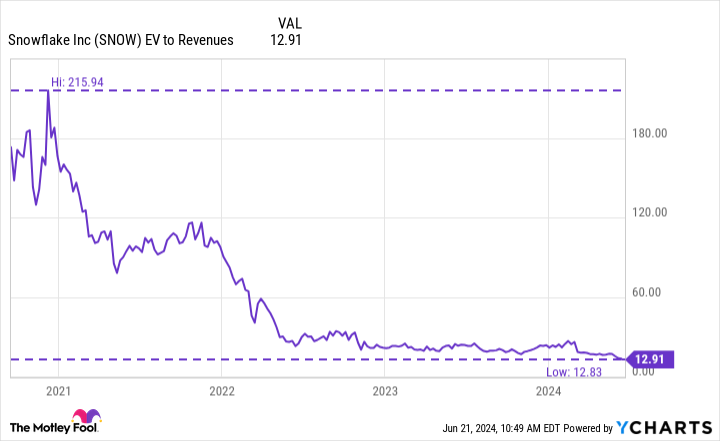

You can see below just how frenzied investors became. Today, there might not be a stock on Wall Street that trades at an enterprise value-to-sales ratio of over 200. It’s an astronomically high valuation!

Interest rates began surging in 2022, which helped dump water on growth stock valuations. Today, Snowflake is trading at a fraction of the valuation it once did and its lowest as a public company. I like to equate a stock’s valuation to investor sentiment. In other words, investors are more pessimistic toward Snowflake today than ever. The question is whether investors should be or if their disdain for the stock is misguided.

Snowflake remains a fundamentally excellent business

Snowflake hasn’t been perfect. The company’s revenue growth was explosive in 2020 but has dramatically slowed. Revenue grew “just” 32% year over year in the most recent quarter, but that’s still enough to put Snowflake among the fastest-growing companies on the market.

Consider just how much Snowflake has grown; the company’s trailing-12-month revenue was roughly $500 million entering 2021, and that’s grown sixfold in just a few years. Snowflake’s customer count has grown from 3,554 to 9,822 during that time. Additionally, the business is very cash-flow profitable, converting a quarter of sales to free cash flow. This is a profitable and growing company that’s thrived despite competition from a privately held adversary in Databricks.

The future looks bright if you believe artificial intelligence (AI) will become crucial to society over the coming decade and beyond. AI trains on data. Snowflake could be essential for customers because it enables companies to organize and search their data and supplement it with third-party data via Snowflake’s marketplace. It could be the ideal platform for companies optimizing their data for AI or the applications they need.

Just look at Snowflake’s stellar net revenue retention rate of 128%, which signals that customers invest heavily in the platform once onboard. Snowflake might not see triple-digit revenue growth again, but it’s clear that it has a path to years, possibly decades, of double-digit growth simply due to how much data there is and will be created moving forward.

The time to shine could be coming

A stock won’t begin to trade higher without increased demand for shares. So, what might be the metaphorical match that lights Snowflake’s powder keg? The company replaced its CEO earlier this year; new CEO Sridhar Ramaswamy is the company’s former VP of AI, which tells investors Snowflake is leaning further into AI.

Snowflake uses a consumption-based billing model. That has hurt the company’s growth over the past several years when companies tightened their wallets under higher interest rates. However, the AI boom could have the opposite effect as companies invest in AI on the platform. You’ll see below that revenue growth bottomed and turned upward last quarter. Investors should pay close attention to this possible turning point in Snowflake’s revenue growth.

In other words, a continued uptick in revenue growth next quarter could spell hope for investors that Snowflake’s growth story is improving again. Only this time, a boost in positive sentiment will come while shares are trading at a depressed valuation compared to where they were in years past.

Ideally, investors think long-term and zoom out to what Snowflake could become five, 10, or 20 years from now. But it’s hard to ignore such a strong company falling so hard while other AI stocks are hitting new highs. A rebound will come down to Snowflake performing well in the future, but the conditions are right for one heck of a comeback story over the next six months and beyond.

Should you invest $1,000 in Snowflake right now?

Before you buy stock in Snowflake, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Snowflake wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $775,568!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 24, 2024

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway, Nvidia, and Snowflake. The Motley Fool has a disclosure policy.

Forget Nvidia: This Young Artificial Intelligence (AI) Stock Is Set to Soar in 2024 was originally published by The Motley Fool