Yves here. Confirming Wolf’s account of the reaction to the unexpectedly strong new jobs report and labor data revisions, the currency market has reacted as if the Fed rate cuts are off the table for now. Emergency market currencies fell markedly.

By Wolf Richter, editor of Wolf Street. Originally published at Wolf Street

Pandemic distortions and millions of migrants suddenly entering the labor market, who are hard to track, have wreaked havoc on labor-market data accuracy.

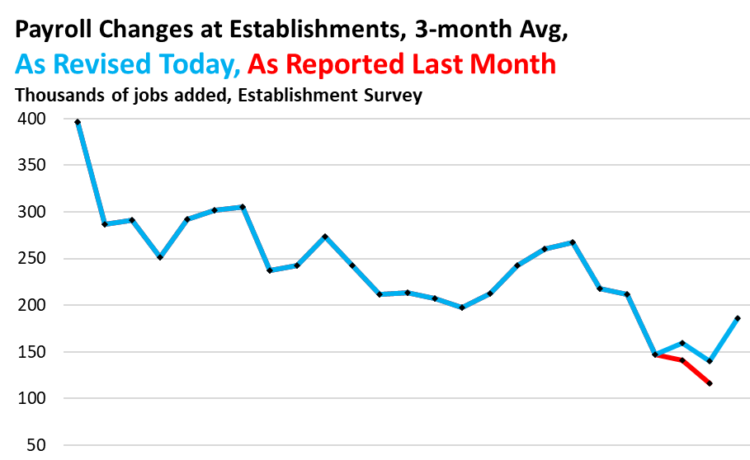

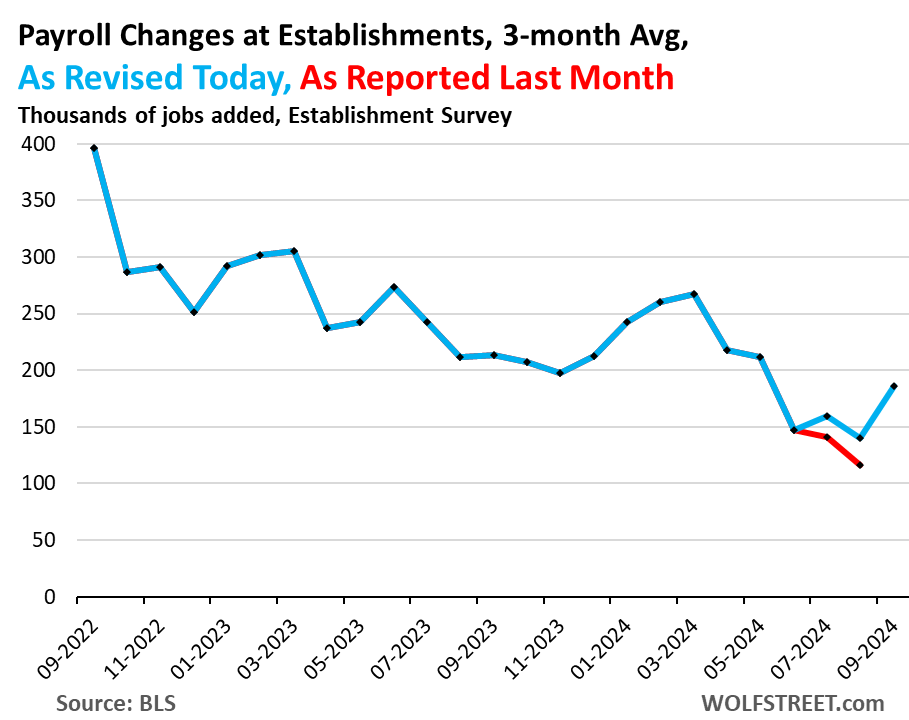

Payrolls at employers rose by 254,000 jobs in September, and the down-revision last month for July was re-revised up a lot, and August was revised higher too, so the three-month average jumped to 186,000 payroll jobs created in September. And the three-month average for August – which had been reported as 116,000 at the time, a scary and sudden deterioration with the revisions that caused so much consternation – was revised up to a half-way decent 140,000.

Turns out, the sudden deterioration of the prior two months were a false alarm. The labor market is just fine, creating a decent but not spectacular number of new jobs, and the unemployment rate dropped for the second month in a row, and wages jumped, and the Fed doesn’t need to cut any further, given the inflation pressures already building up again — though it will likely cut further, though maybe at a slower pace than previously anticipated.

The blue line shows the three-month average of jobs created as reported today. The red segment shows the three-month average as reported a month ago:

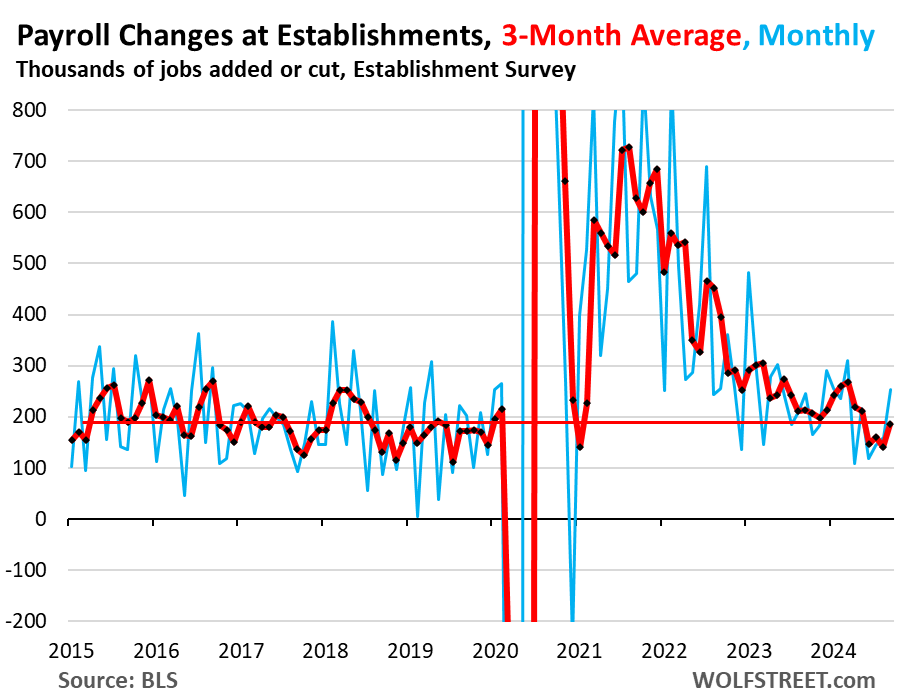

Here is the long view, as revised: The three-month average is right in the sweet-spot of the strong labor market in 2018 and 2019.

Clearly, the frenetic pace of hiring after the pandemic is over, and the labor shortages are over. The pace is back to a healthy strong job growth.

This picture matches other data showing that layoffs and discharges remain very low. Companies in aggregate are creating jobs at a decent pace, and they’re hanging on to the employees they’ve got.

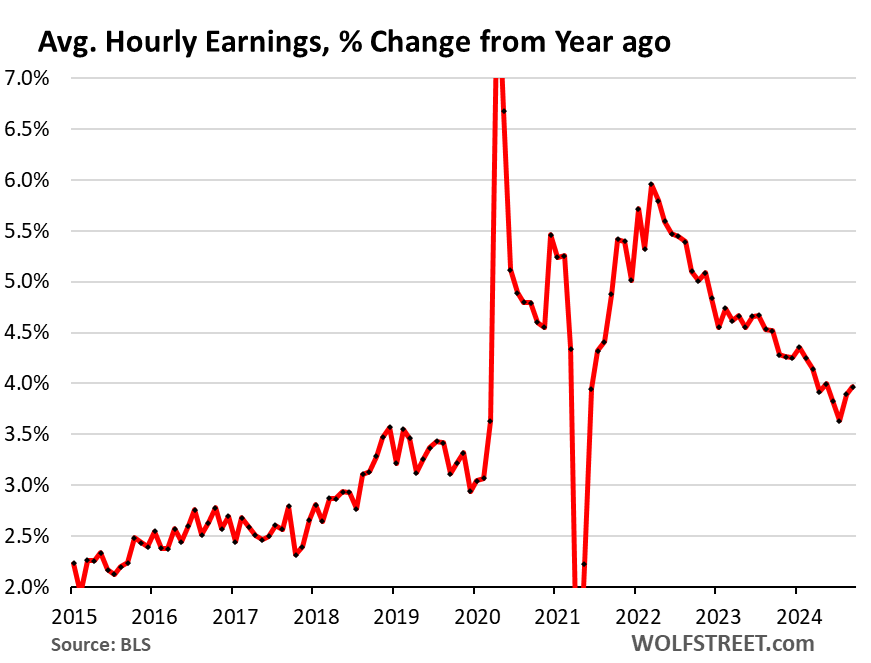

Average hourly earnings were also revised higher for August to a hot 5.6% month-to-month annualized, from 4.9%. And in September, they increased by another 4.5% annualized from the upwardly revised August, which caused the three-month average to increase by 4.3%, the highest since January. The three-month average has been increasing steadily since April (red line). This is based on the survey of establishments.

The 12-month increase of average hourly earnings rose to 4.0% in September, and August was revised higher to 3.9% (from 3.8% as reported a month ago). Those two months combined show the fastest acceleration since March 2022, and are well above the peaks of the 2017-2019 period.

So in terms of inflation – and what the Fed has been worrying about – this accelerating wage growth is not going in the right direction anymore.

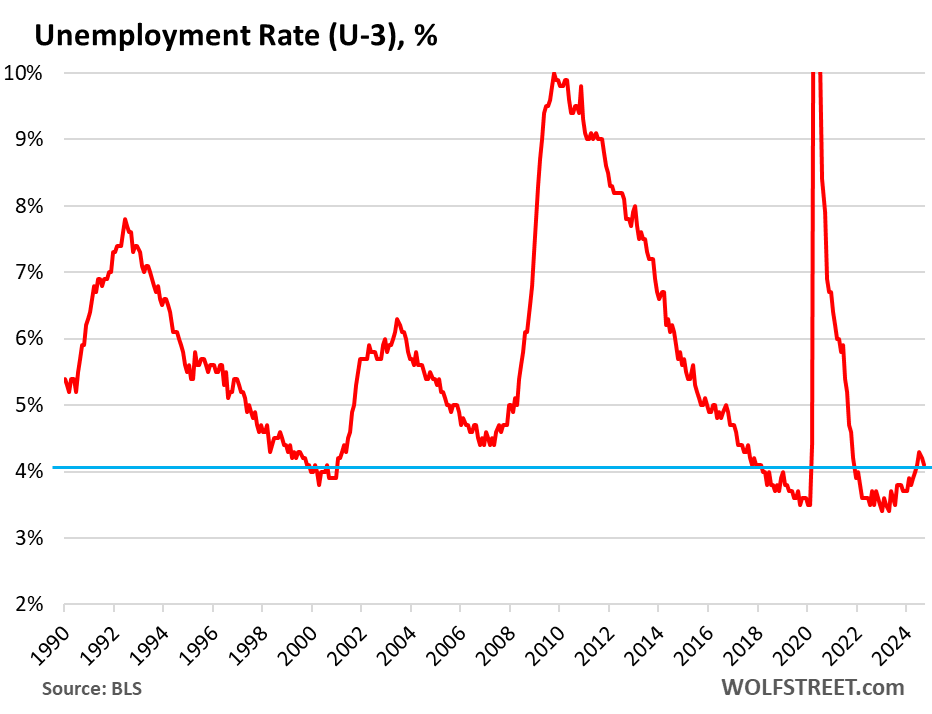

The headline unemployment rate (U-3) dipped to 4.1%, the second month in a row of declines. 4.1% is historically low, but is up from the period of the labor shortages in 2022. This is based on the survey of households.

The unemployment rate is now below the Fed’s 4.4% median projection for the end of 2024 and for the end of 2025, according to the Fed’s Summary of Economic Projections released at the rate-cut meeting.

The weakening of the labor market that the Fed projected in justifying the 50-basis point cut has reversed, been revised away, or failed to happen.

The unemployment rate is also where the massive influx of immigrants over the past two years – estimated at 6 million in 2022 and 2023 by the Congressional Budget Office – shows up: Those that are looking for a job but have not yet found a job count as unemployed. And their influx into the labor force has caused the unemployment rate to rise from the lows last year.

A rise of the unemployment rate caused by a surge in the supply of labor is a different dynamic than a rise of the unemployment rate caused by job cuts and a reduction in demand for labor, as we would see during a recession:

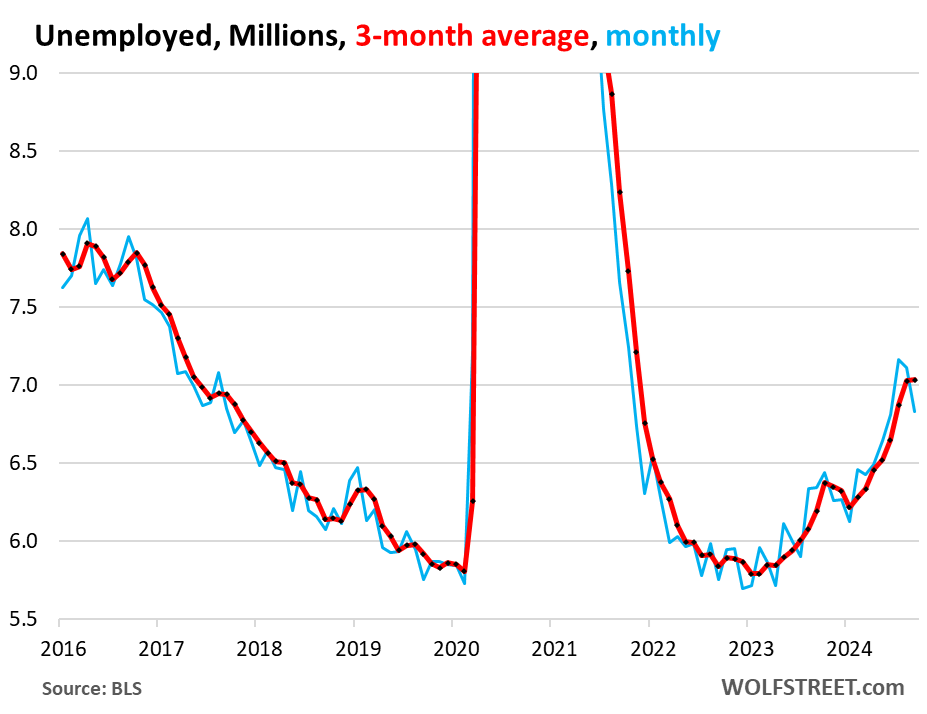

The number of unemployed people looking for a job fell for the second month in a row, to 6.83 million. The three-month average inched up to 7.04 million.

The unemployment rate (chart above) accounts for the large-scale growth of the population and of the labor force over the decades. This metric here of the number of unemployed does not take into account the growth of the population and the labor force, and over the decades, a growing population and labor force entails a growing number of people looking for a job.

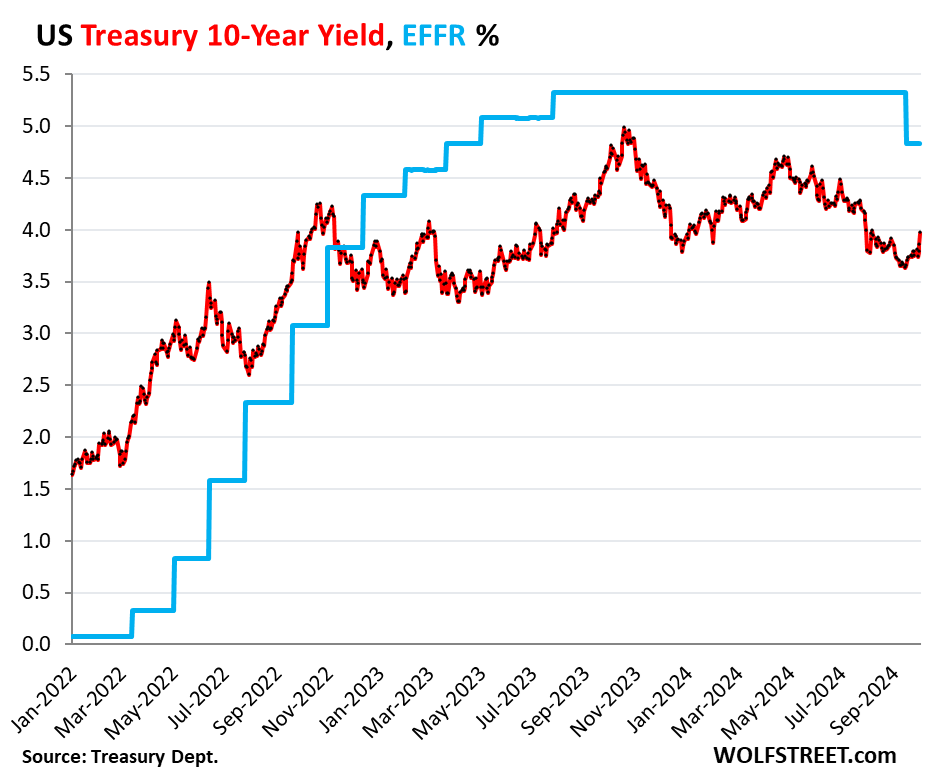

And the bond market woke up.

Upon the news that the labor-market scare last month was a false alarm, and that aggressive rate cuts to save the labor market are not needed, and that wage growth is contributing to general inflation concerns that we have already seen in the Consumer Price Index for August and July, and in what companies have said about raising their prices, and in the pricing power that companies still exert…

Well, upon the news, the bond market woke up, and the 10-year yield jumped by 12 basis points to 3.97% at the moment, the highest since August 8. Since the rate cut, the 10-year Treasury yield has risen by 27 basis points.