Nike (NYSE: NKE) reports quarterly earnings on a different schedule than most public companies, and its updates often give the market a sense of what’s happening in retail before they get other earnings announcements. Because Nike plays such a strong role on the retail scene, its performance can be a harbinger of what’s to come. For example, at the end of 2021, it was Nike that gave some of the earliest indications of the supply chain crisis that ended up afflicting retailers and shaking up the economy.

So it comes as no surprise that after a concerning report from Nike at the end of June, investors have become pessimistic about other companies as well. Lululemon Athletica (NASDAQ: LULU), one of Nike’s main challengers over the past few years, has demonstrated resilience and hasn’t changed its outlook, but its stock has plunged 17% since Nike’s update. Is there anything to be concerned about? Or is Lululemon stock flashing a big buy signal?

Is what’s bad for Nike bad for Lululemon?

Nike’s update for the 2024 fiscal fourth quarter (ended May 31) had two sides. One was negative news relating to its own business, and the other was negative news related to retail in general. Most of its problems related to its own business, but management cited “macro uncertainty” as a continuing issue. Nike has been particularly impacted by ongoing pandemic-driven problems in China, where it had high promotional activity to sell off inventory. It has a broad strategy targeting several areas to generate higher sales and expand its margins.

This is a difficult time for Nike, which attracts interest from a broad spectrum of demographics. Inflation is leading its mass-market consumers to cut spending, and they might be switching to lower-priced brands, while its affluent customers may be swayed by new, premium brands like the fast-growing On Holding or by athlete-focused brands like Brooks (owned by Berkshire Hathaway).

But is this another signal of what’s coming for other large athletic brands?

Trouble brewing?

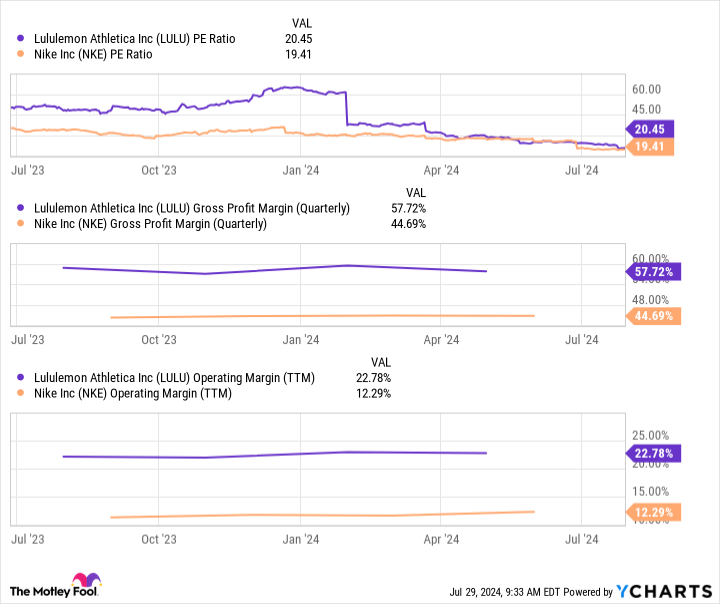

Lululemon’s most recent update was for the 2024 fiscal first quarter, ended April 28, a period similar to Nike’s fourth quarter. Revenue increased 10% year over year, and it enjoyed a 0.2-point increase in its gross margin to 57.7%. Operating margin decreased by 0.5 points, but earnings per share rose from $2.28 to $2.54. All in all, it was a good quarter.

Management mentioned some of its own difficulties in the quarter. It said things got off to a slow start because of several missed opportunities related to colors in women’s apparel and handbags as well as a narrow selection and low inventory in some of its basic products. However, company leaders felt like they were on top of the situation and were correcting it. The market didn’t have any quibbles with management’s update, and Lululemon stock remained steady after the report.

Lululemon has several things in its favor that Nike doesn’t. For example:

-

It’s underpenetrated internationally, where it’s growing faster than in the U.S. International sales increased 35% year over year, and generating higher international sales is an integral part of its growth strategy.

-

It’s also positioned and priced as a more premium brand than Nike, and its more affluent target market is more resilient despite inflation.

Recently, however, Lululemon gave another update about a product issue. It’s pausing sales of a new product line with a fabric called Breezethrough because customers are finding the designs unflattering. (I would note, in Lululemon’s favor, that the product was only released in early July.) That’s a pretty fast reaction to consumer feedback. It’s not the first time Lululemon has misstepped with a new product, but the company bounced back then, and it should bounce back now.

This, along with its previous product issues and the dynamic operating environment, precipitated a Wall Street analyst downgrade, and Lululemon plummeted further.

Time to buy Lululemon stock?

At the current price, Lululemon stock trades at a P/E ratio of 20, nearly as low as Nike’s (and nearly its lowest level in 10 years), even though it’s growing much faster, has a stronger direct-to-consumer business, and boasts a much higher gross margin and operating margin.

It looks like Lululemon is in a strong position right now, and at the current price, it could be considered a bargain. Investors should go in with their eyes open and understand the context in which Lululemon is operating right now — I’m not erasing its challenges. However, it’s performing well under pressure and has many merits that one would want in an excellent long-term holding.

There’s a chance that Lululemon stock could continue to slide, and it will if the business doesn’t meet Wall Street’s expectations in its next quarterly update. But you can’t time the market, and if the company does come through on its guidance, the stock will start a new climb. As long as you can handle some potential near-term volatility, now is a great time to buy Lululemon stock.

Should you invest $1,000 in Lululemon Athletica right now?

Before you buy stock in Lululemon Athletica, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lululemon Athletica wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $669,193!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 29, 2024

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway, Lululemon Athletica, and Nike. The Motley Fool recommends On Holding and recommends the following options: long January 2025 $47.50 calls on Nike. The Motley Fool has a disclosure policy.

Lululemon Stock Flops After Nike News. Why It Could Be a Great Time to Buy was originally published by The Motley Fool