(Bloomberg) — Hedging is back as investors fret over concerns about everything from the US presidential election to second-quarter earnings, economic growth and interest rates.

Most Read from Bloomberg

The Cboe Volatility Index, a gauge of options prices, surged the most in more than a year last week as stocks sank with growing calls for Joseph Biden to quit the presidential race. Now that he’s done so and thrown US politics into uncharted territory, futures on the gauge have slipped after earlier climbing as much as 1.8% in Asian trading. October contracts, which measure swings around the vote, rose even more and were still up by 1:19 p.m. in Hong Kong.

Also read: Dollar Slips as Biden Quits Race, China Bonds Gain: Markets Wrap

Should Vice President Kamala Harris become the Democratic nominee, risk pricing is likely to look similar to what it was before Biden’s debate against Donald Trump, according to Stuart Kaiser, head of US equity trading strategy at Citigroup Global Markets.

“Policy continuity means she is the closest proxy for Biden among the alternatives so the volatility pricing will look very similar,” Kaiser said. “Perhaps with a bit more risk premium given the late change and recent events on the Trump/GOP side of things.”

After shunning protection against a selloff that never happened in the first half of the year, traders are now switching modes. Beyond politics, they’re watching whether technology company earnings can support still-lofty valuations — Tesla Inc. and Google’s parent Alphabet Inc. are reporting this week — while chatter on when the Federal Reserve will start to lower interest rates will remain in focus.

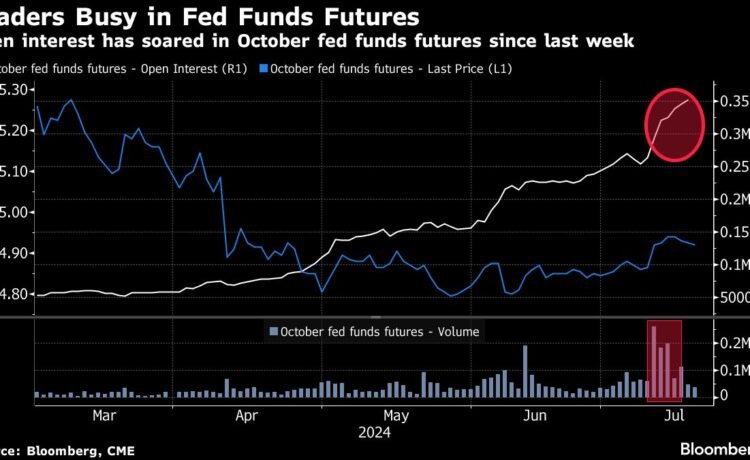

With increased chances of Trump winning the presidency largely baked in, positioning in the rates market is shifting to gauge the chances of a cut at the end of this month or a bigger one in September.

Some of the froth has come out of the stock market as earnings ramp up. Just a couple of the biggest tech companies have a positive call skew — when bullish options are more expensive than bearish ones — according to Scott Nations, president of volatility and options index developer Nations Indexes. That’s a sharp change from earlier this month, when seven out of the top 10 stocks in the S&P 500 did, he said.

“It seems investors have finally figured out that stocks can go down too and want protection,” Nations said.

The VIX ended last week at its highest level since April, and the cost of options on the gauge — often used to hedge against sharp market selloffs — also hit a three-month high. More than 170,000 August calls betting the VIX would go to 21 traded, for a level the index hasn’t reached since October.

When it comes to equity options, not only have puts been bid up, but calls are also under pressure, according to Nations. His company’s index of call volatility was down 6.3% on Friday. That may be a sign traders are willing to risk being short bullish contracts, expecting implied volatility to ease if the S&P 500 rebounds.

In Treasury futures, large short positions were unwound in the long end of the strip on Wednesday, helping flatten the curve in an indication that investors were starting to lose patience with the so-called Trump steepener trade. The shift may be an indication that the Treasuries curve looks more likely to be driven in the near term by Fed monetary policy rather than swings in odds for a Trump presidency.

In options linked to the Secured Overnight Financing Rate, which closely tracks policy expectations, traders are protecting for a tail risk of a half-point rate move by the September meeting versus swaps pricing a quarter-point change. The hedges would cover dovish scenarios such as a quarter-point rate-cutting cycle starting as early as this month, a July hold and fifty-point move in September, or any inter-meeting move during the extended seven-week period between July and the September gathering.

While it’s still too early to tell whether the shift in positioning will last, the quieter summer days may exaggerate moves.

“The market has been conditioned to buy the dip and volatility mean reverts quickly, but high market concentration is a risk,” said Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence. “The summer period, when liquidity can be light, can leave the market more exposed than usual to headlines.”

–With assistance from Edward Bolingbroke and Natalia Kniazhevich.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.