After a rebound year in 2023, the tech sector continued its momentum through the first half of this year. Notable tech-heavy indexes like the Nasdaq Composite and Nasdaq-100 are up around 20% and 19%, respectively, largely due to the growth of big tech stocks.

Like most stocks associated with artificial intelligence (AI), Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL) has benefited from the technology’s ushering into the mainstream. Alphabet’s stock is up close to 32% this year and reached a new all-time high in late June.

When stocks are flirting with peaks, many investors become hesitant, fearing a correction could be in the works. Whether that happens remains to be seen, but as a long-term investor, I’m doubling down on Alphabet, and here’s why.

Google will remain the king of search advertising

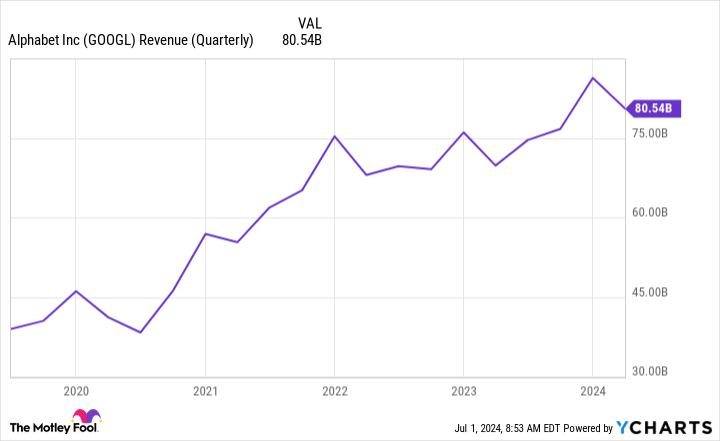

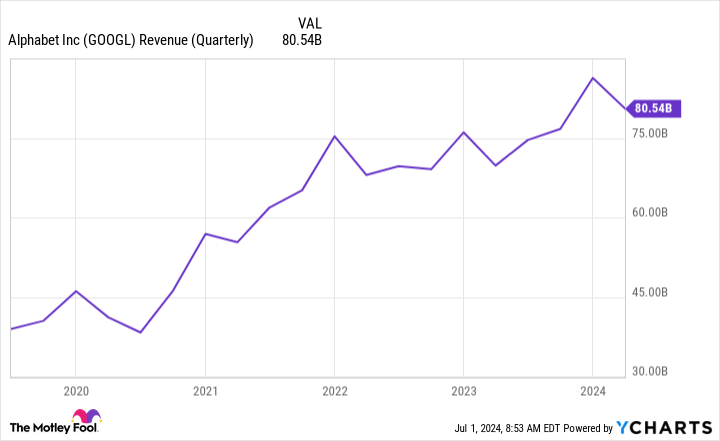

Alphabet’s bread and butter has been and will continue to be money earned from Google advertising. In the first quarter, Alphabet made $80.5 billion, and Google advertising accounted for over 76% of it. The good news, though, is that it’s less than in previous quarters, a signal that it’s becoming less reliant on it.

Concerns about how new AI implementation may affect Alphabet’s advertising revenue are valid but overblown. On one end, Google makes money when users click links on their search ads, so if users get their questions answered by Google’s AI Overview answers, then a slowdown is possible.

On the other hand, AI inclusion also opens up new advertising opportunities with new ad formats. Google advertising is so important to Alphabet’s business that you have to assume the company wouldn’t overlook the effect of its AI Overview implementation.

When you routinely have around a 90% market share in online search, you have more room to experiment and discover ways to enhance user engagement and create more targeted advertising opportunities.

Google Cloud could be a huge growth area

The cloud computing industry is rapidly growing, and many assume AI advancements will add to the momentum. Google Cloud is still a ways behind leaders Amazon Web Services (31% market share) and Microsoft Azure (25% market share) in terms of adaptability, but the platform has turned the corner on profitability and should contribute to growing margins.

Cloud platforms have a lot of fixed costs, such as data center operations and other infrastructure-related expenses. This means it takes a certain scale before the platforms achieve sustainable profitability. Now that Google Cloud has seemingly crossed that threshold, it should see a financial boost from a segment that was once weighing down its margins.

Google Cloud revenue in the first quarter was $9.6 billion, up $2.1 billion from last year. Its operating income (profit from its core operations) had a more dramatic jump, increasing over 370% year over year. This increased efficiency helped increase Alphabet’s operating margin to 32% from 25% last year.

Alphabet seems to be the best value in big tech

The “Magnificent Seven” is a phrase coined to describe seven of the world’s most influential tech companies. They include Microsoft, Apple, Nvidia, Amazon, Meta Platforms, Tesla, and Alphabet. As they go, so does the tech sector, for the most part.

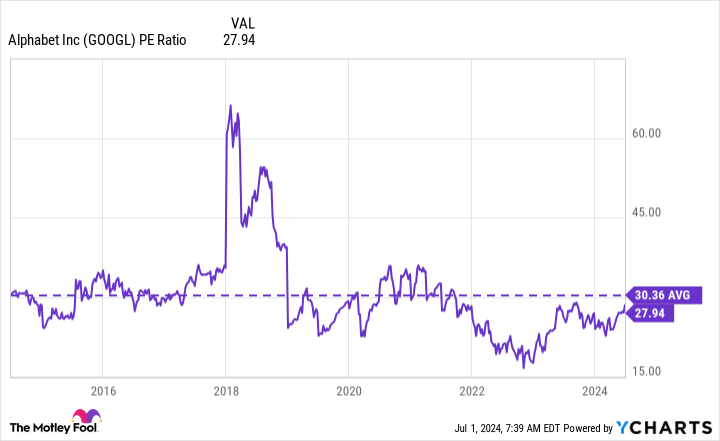

Alphabet seems to be the “cheapest” of the bunch, with a price-to-earnings (P/E) ratio of just under 28. Being the cheapest of the Magnificent Seven doesn’t automatically make Alphabet cheap because those stocks are routinely priced at a premium, but Alphabet is cheaper than its average for the past decade.

This could be a great chance for investors to grab a piece of a world-class company at a fair valuation. Alphabet has strong growth prospects, so it’s easy to justify its valuation for long-term investors. This growth won’t happen overnight, but Alphabet’s newly announced dividend should buy some patience from investors.

The quarterly dividend is $0.20, with a yield below 0.5%, so it’s not necessarily a must-have for income-seeking investors. Still, initiating a dividend program at all should signal Alphabet’s confidence in its financial health and ability to sustain long-term profitability.

Should you invest $1,000 in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $751,670!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 2, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Stefon Walters has positions in Apple and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Alphabet Stock Soars to New Peak. Here’s Why I’m Doubling Down. was originally published by The Motley Fool