Tesla (NASDAQ:TSLA) stock has gained in recent weeks after beating delivery expectations in the second quarter. The Elon Musk-run company has seen its shares rise 40.9% over the past 30 days and now trades with some enormous valuation multiples. I’m still neutral on Tesla, as I appreciate that Robotaxi and robotics could be game-changing for the business, but the valuation is hard to justify.

A Resurgent Tesla

In Q2, Tesla’s deliveries were down by 4.8% year-over-year (YoY), but this was better than the market expected. In the three months to June 30, Tesla delivered 443,956 vehicles, representing a 14.8% increase versus the first quarter. The stock has surged since, with positive figures across the electric vehicle (EV) sector inferring resurgent demand.

Tesla stock had already started pushing upward in June after shareholders voted in favor of giving Musk his 2018 $56 billion pay package and reincorporating the company in Texas. The news led Tesla shares to jump more than 10%, taking it above $200 a share.

Is Tesla’s Surge Justified?

As a manufacturer of cars, Tesla is clearly overvalued. Even Elon Musk has asked investors to value Tesla as a robotics or artificial intelligence (AI) company rather than one that purely focuses on the production of road vehicles – even if they are electric. As such, some analysts may question why Tesla, which was already trading on elevated multiples, has surged on the back of these improved EV deliveries. It’s a good point.

The stock is currently trading at 96.4x non-GAAP forward earnings, making it the most expensive EV stock by many multiples and one of the most expensive technology companies. Moreover, the expected earnings growth rate for the next three to five years is just 11.2%, inferring that analysts see very little tangible impact from the Robotaxi business over the medium term.

In turn, this leads to a price-to-earnings-to-growth (PEG) ratio of 8.7x. That’s far beyond what is normally considered attractive (1.0x or lower).

Other metrics compound this unattractive valuation. The stock trades at 8.3x TTM sales and 7.9x forward sales, representing an 830% and 813% premium to the sector, respectively. Tesla’s forward price-to-cash-flow ratio of 63.9x also represents a 585% premium to the sector as a whole.

However, Musk has been touting two major developments, which are due to take place over the next 18 months. The first is the long-awaited Robotaxi – set to be unveiled on August 8 – and the second is the sale of its Optimus robots, which may start in the second half of 2025.

What Could These Developments Mean for Tesla?

Autonomous driving offers Tesla the opportunity to dominate in a new and exciting segment. Looking from the outside, Tesla appears to be ahead of the game when it comes to automation. We’ll learn more on August 8. Even Nvidia (NASDAQ:NVDA) CEO Jensen Huang agrees, recently noting that Tesla was “far ahead” in self-driving tech.

The Robotaxi will allow Tesla to open up new revenue streams. Unsurprisingly, one of these would be ride-hailing. In 2023, 76% of Tesla’s revenues were generated through car sales, with a further 8% generated through servicing. Just 5.8% or $6 billion was earned through its Energy Generation and Storage division. Ride-hailing also promises wide margins.

Despite the potential of the Robotaxi, I’ve seen very few analysts’ forecasts that actually seek to quantify this potential. Cathie Wood’s ARK is one exception. According to ARK Invest, nearly 90% of Tesla’s earnings will be attributed to the Robotaxi business in 2029. In ARK’s bear-case scenario, the autonomous ride-hailing business would deliver $603 billion in 2029. In its bull case scenario, this figure rises to $951 billion. In turn, this led Wood’s investment fund to suggest the stock will be worth $2,600 in 2029.

It’s worth recognizing that ARK Invest’s forecasts have been dismissed by many as over-ambitious. For one, the global ride-hailing market is expected to be worth $215.7 billion by 2028 (according to Statista). That’s less than half what ARK believes Tesla would generate from ride-hailing in its bear case for 2029. I can only assume that Wood’s fund is inferring that self-driving vehicles will engender a huge shift away from car ownership towards ride-hailing.

There are also question marks as to how Tesla could mass-produce a fleet of Robotaxis large enough to generate the figures projected by ARK. Assuming a production cost between $150,000 and $200,000 (per ARK Invest), building a global fleet of Robotaxis would likely cost trillions. Tesla doesn’t have the necessary cash flow to build a global fleet.

Since the Q1 results, Musk has also been touting Tesla’s potential in robotics, with “limited production” of its Optimus robot in 2025. According to Musk, robots could turn Tesla into a $25 trillion company. However, investing in Tesla for its robotics capabilities could be very speculative, considering how little we know.

Is Tesla Stock a Buy, According to Analysts?

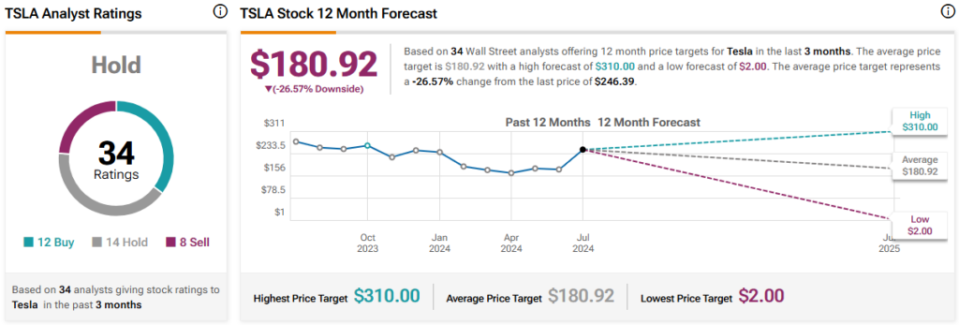

On TipRanks, TSLA comes in as a Hold based on 12 Buys, 14 Holds, and eight Sell ratings assigned by analysts in the past three months. The average Tesla stock price target is $180.92, implying 26.57% downside potential.

The Bottom Line on Tesla Stock

Despite Tesla being in a pole position to dominate in the autonomous era, I remain wary of Musk’s overpromising. This makes it very hard to get behind a stock that’s currently trading at 96.4x non-GAAP forward earnings. It could be priced for perfection, and if Musk underdelivers on August 8, the share price may pull back significantly. That’s why I’m remaining neutral.