Companies today generate mountains of data. That data can be of great value — but only if it’s correctly harnessed, visualized, and used to improve decision-making. Often, though, that data lives in a variety of different software systems, with various chunks siloed away in platforms that can’t communicate with each other, complicating any effort to see the full picture. For instance, a corporation may have a customer services database, enterprise management software, a marketing platform, and more. Unifying the data from all of these platforms into one system and mining the integrated result for actionable insights is Palantir‘s (NYSE: PLTR) specialty, and why its services are in demand.

The Palantir Artificial Intelligence Platform (AIP) is its latest innovation, and it’s loaded with potential.

Clients are flocking to Palantir AIP

Imagine a wholesale supplier facing a severe weather event affecting one of its centers. Management needs to know the most efficient alternative methods for keeping its customers supplied, and what effect its choices will have on margins. Or perhaps you manage planning a company’s inventory levels, and you need to know what impact a price increase or decrease will have on demand. Or you want to automate your payment processing to suppliers by unifying documents like purchase orders, invoices, and warehouse receipts. These are all use cases for Palantir’s AIP.

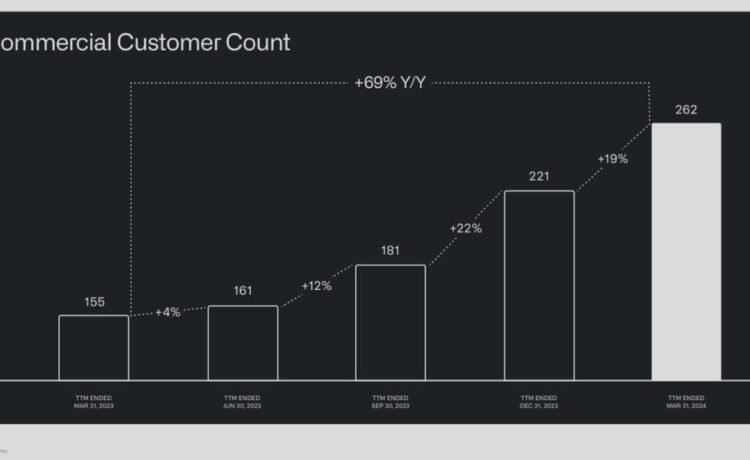

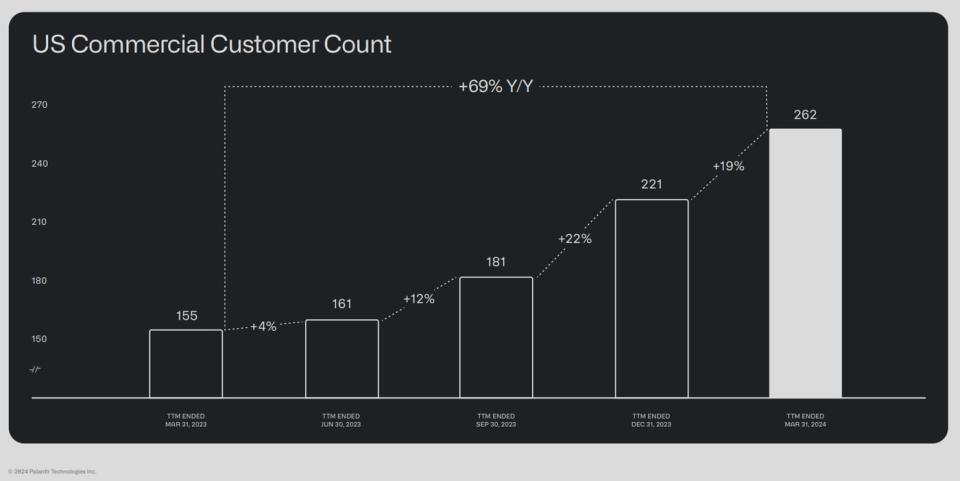

AIP uses large language models that enable its clients to ask questions like those in plain English and receive actionable responses. Selling a platform this complex is difficult. Examining use cases for other companies is helpful, but it is still difficult to visualize how a platform like AIP will work in a specific company. Because of this, Palantir conducts “boot camps” where potential customers build use cases unique to their businesses in just days. These have proven a terrific tool to increase Palantir’s client base — its U.S. commercial customer count is exploding.

In the first quarter, that translated to a 40% year-over-year increase in U.S. commercial sales to $150 million and 27% worldwide commercial sales growth to $299 million. Government revenue grew by a slower 16% to $335 million. Penetrating the commercial market will be critical to Palantir’s long-term success.

Total sales in Q1 rose 21% year over year to $634 million, and Palantir increased its profitability. But not everyone is convinced.

Examining the Palantir bear case

Palantir enjoys a large following among retail investors, and has inspired spirited debates between its bulls and bears over the last several years. The company is methodically putting many of the bear arguments to bed. I’ll take you through two of them.

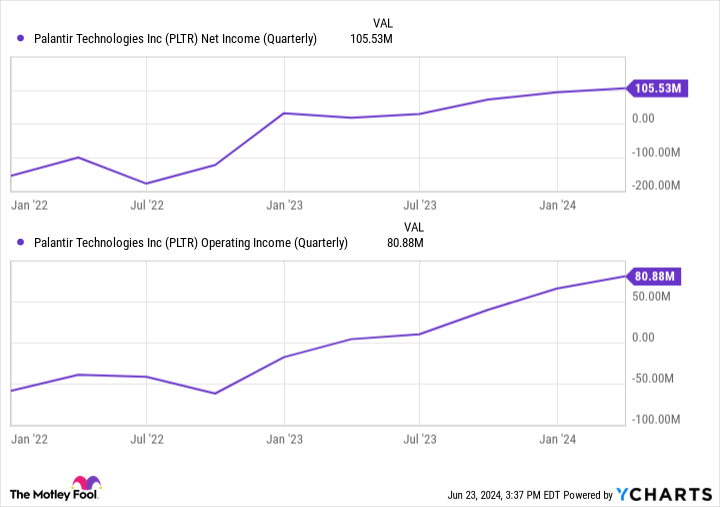

First, many lamented the company’s persistent unprofitability. This was legitimate criticism as the company racked up annual losses until 2023, when it achieved profitability. Palantir has posted net profits in the last six quarters and dramatically increased operating profits.

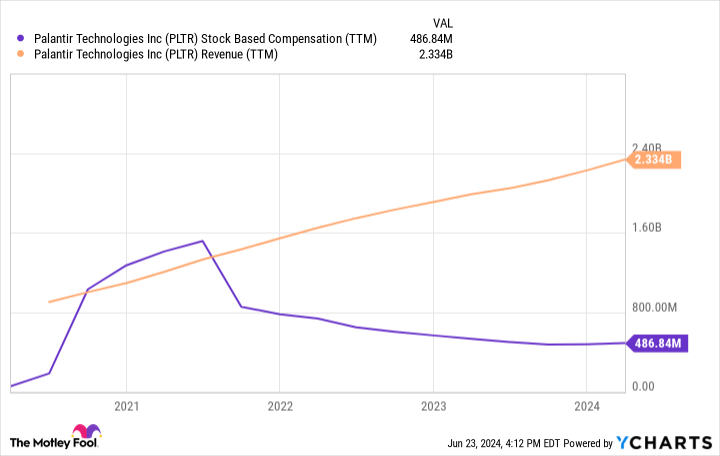

Second, Palantir bears pointed out the company’s extensive use of stock-based compensation to reward employees. The most significant portion of such distributions usually goes to the top executives. The result of issuing a large number of new shares to pay your team, however, is that the number of outstanding shares increases and shareholders’ portions of the pie decrease. However, Palantir has been dialing back its stock-based compensation as its revenue has been ramping up.

Using stock-based compensation also helps companies preserve their cash. Palantir finished Q1 with $3.9 billion in cash and investments on its books and no long-term debt.

Is Palantir stock a buy?

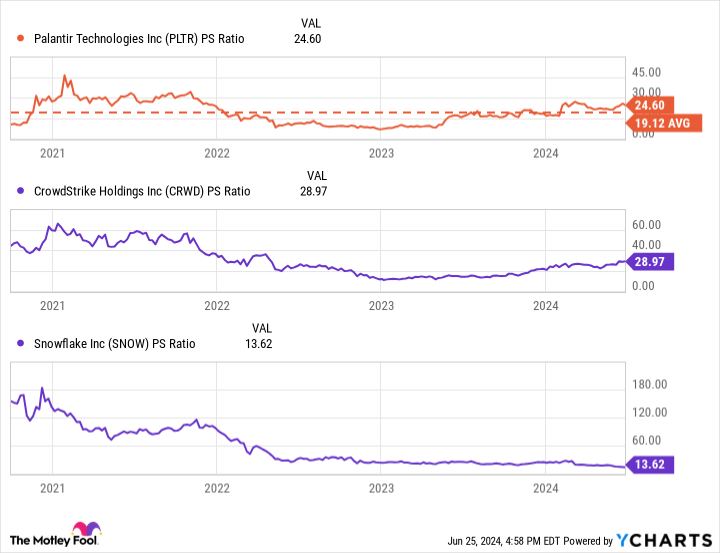

Another reason some investors remain in the Palantir bear camp is its high valuation. The stock trades at nearly 25 times current sales. That’s a lower price-to-sales ratio than CrowdStrike and a higher one than Snowflake — both of which, like Palantir, are high-growth software companies with market caps below $100 billion.

The stock is also trading at a higher valuation than its historical average. However, Palantir is the most profitable of these three tech companies. Over its last four reported quarters, Palantir produced nearly $200 million in operating profits, compared to $24 million for CrowdStrike and a loss of $1.2 billion for Snowflake.

Investors can afford to be patient if they choose to buy Palantir stock. The best strategy would be to build your stake in it gradually and regularly over time so you can take advantage of any dips in the price that might occur. A dollar-cost averaging strategy can reduce short-term risk when investing in high-priced stocks.

Palantir has entrenched itself as a leader in data and artificial intelligence management. Although its valuation is high, its profits are growing and it’s in a strong financial position to excel over the long term.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $759,759!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 24, 2024

Bradley Guichard has positions in CrowdStrike. The Motley Fool has positions in and recommends CrowdStrike, Palantir Technologies, and Snowflake. The Motley Fool has a disclosure policy.

Palantir’s Untapped Potential: Decoding the Artificial Intelligence (AI) Stock’s Long-Term Value for Strategic Investors was originally published by The Motley Fool